India’s healthcare landscape is undergoing a dramatic transformation. For decades high-quality medical care was concentrated in metropolitan hubs like Delhi, Mumbai & Bengaluru forcing patients from smaller towns to travel long distances for specialised treatment. But that narrative is fast changing. Today leading private hospital chains are moving decisively into Tier II & Tier III cities bringing advanced healthcare services closer to where people actually live.

This shift is not just about adding more hospital beds it reflects deeper structural changes: rising health insurance coverage, increasing affordability, growing burden of non-communicable diseases (NCDs) & emergence of medical technology that enables remote care. Backed by strong balance sheets, private equity capital & government support through schemes like Ayushman Bharat India’s hospital chains are entering an aggressive expansion phase.

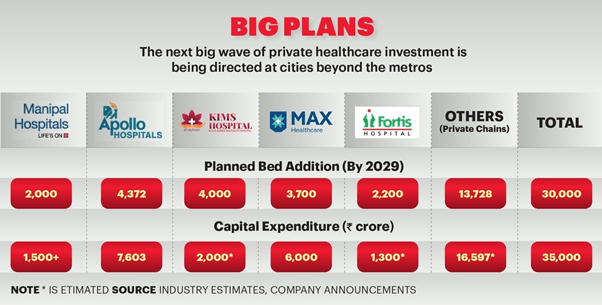

Over next four to five years private players are expected to add 30,000+ new beds with an investment of nearly ₹35,000 crore targeting emerging healthcare hubs beyond metros. Whether through acquisitions, brownfield expansions, or new greenfield projects these networks are laying foundation for a more inclusive healthcare system one where world-class oncology, cardiology, neurology & transplant care is no longer restricted to India’s largest cities.

In December 2023, a quiet revolution took shape in Lucknow. Max Healthcare, one of India’s largest hospital groups, acquired 550-bed Sahara Hospital in a ₹940 crore deal, renaming it Max Super Speciality Hospital, Lucknow. For residents like 51-year-old Rekha Mishra, a schoolteacher battling chronic health issues, move brought much-needed relief. Until then, she had to travel to Delhi for advanced medical treatment.

This single acquisition was not just about one hospital or one city. It represents a larger trend sweeping across India’s healthcare landscape: private hospital chains are moving aggressively into Tier II & Tier III cities. Armed with capital, technology & strategic intent, they are building new capacities & rebalancing geography of healthcare access.

A Wave of Expansion: Beds, Capital & Beyond

According to industry estimates, private hospital chains plan to add over 30,000 new beds in next 4–5 years, with a capital commitment of around ₹35,000 crore. This is arguably next big wave of private healthcare investment in India—targeted not at metros but at state capitals, industrial hubs & smaller cities.

Examples of Big Bets

- Max Healthcare: Post its Lucknow entry, group has lined up ₹1,500–2,500 crore investment in Uttar Pradesh, including a 265-bed expansion at current facility & a new 500-bed hospital along Shaheed Path.

- KIMS Hospitals (Telangana): Planning to add 4,000 beds with a ₹2,000 crore internal investment.

- Aster DM Healthcare: Committing ₹1,900 crore to expand over 2,100 beds organically & an additional 1,200+ via merger with Quality Care India Ltd (QCIL).

- Apollo Hospitals: Rolling out 4,372 beds across next 3–4 years with a project outlay exceeding ₹8,000 crore, largely funded by internal accruals. Upcoming projects include facilities in Gurugram, Pune, Varanasi, Lucknow & an expansion in Mysuru.

- Manipal Hospitals: Recently acquired Sahyadri Hospitals in Maharashtra, taking its capacity to ~12,000 beds & 49 hospitals. It has 1,400 beds under development in Karnataka, Maharashtra & Chhattisgarh, with further plans in Kerala, Telangana, NCR & Eastern India.

- Fortis Healthcare: Adding 2,000 beds through brownfield expansions in Noida, Faridabad & Gurugram, while integrating Punjab’s Shrimann Superspecialty Hospital into its growing network across Ludhiana, Amritsar, Mohali & Jalandhar.

What’s Driving Expansion?

1. Rising Burden of Chronic Diseases

- Non-communicable diseases (NCDs)—heart disease, diabetes, cancer, respiratory illnesses—are now leading cause of mortality in India.

- WHO notes cardiovascular diseases alone account for 28% of deaths in India.

- Apollo, Fortis, Manipal & Aster are all ramping up oncology, cardiac, neuro & transplant care. Oncology already contributes 15.5% of Fortis’s revenue.

2. Insurance & Affordability Factor

- Expanding health insurance coverage (Ayushman Bharat, employer-backed, private health insurance) is making specialised care financially viable in smaller towns.

- Rising disposable incomes in Tier II/III cities are changing demand patterns.

3. Real Estate & Scalability

- Land availability is more affordable outside metros, lowering entry barriers.

- Brownfield acquisitions (like Max in Lucknow, Manipal in Pune, Fortis in Punjab) allow rapid scaling without time lag of greenfield projects.

4. Medical Tourism & International Demand

- India’s medical tourism market ($21B in 2024) is projected to grow to $70.9B by 2033 (CAGR 13.8%).

- Patients from Bangladesh, Middle East, Africa & Southeast Asia seek high-quality yet affordable care.

Tech-Led Healthcare: Silent Expansion

Physical infrastructure isn’t only focus. Digital healthcare delivery models are transforming access:

- Manipal Hospitals: Dual expansion model—physical + virtual. Telemedicine, remote monitoring & home care reduce re-admissions.

- Fortis Healthcare: Linking smaller centres to city-based specialists using digital networks.

- Apollo Hospitals:

- Apollo 24/7 integrates teleconsults, diagnostics & pharmacy.

- Over 1 million teleconsults annually.

- Apollo TeleHealth runs India’s largest rural telemedicine network.

- Aster DM Healthcare:

- Aster Health App enables consultations, bookings & soon pharmacy services.

- Cloud-based electronic health records + AI diagnostics.

- Aster@Home delivers nursing, physiotherapy & remote chronic care.

Technology is helping these groups reach more patients with fewer doctors, ensuring continuity of care independent of geography.

Capital Game: PE, Internal Accruals & M&A

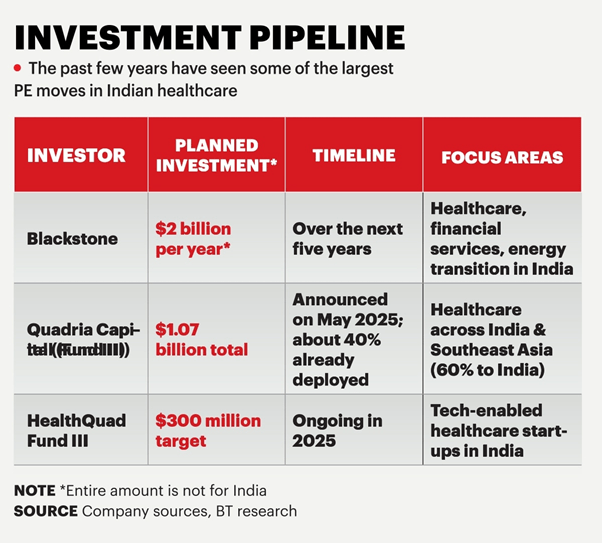

Private Equity Backing

- Temasek: Increased stake in Manipal to 59% (April 2023, ~$2B deal).

- Blackstone: Invested ₹6,000 crore across hospital assets (Oct 2023).

- Mubadala, Novo Holdings, CalPERS: Acquired 8% in Manipal for $400M (Feb 2024).

Self-Financing Strength

- Apollo Hospitals: Funding its ₹8,000 crore plan mostly via internal accruals.

- Fortis Healthcare: Core expansion is internally financed; raised ₹1,550 crore via NCDs in 2024 for diagnostics consolidation.

- Aster: Post-QCIL merger, stronger cash flows support expansion.

This balance between external PE capital & internal cash strength provides resilience.

Challenges Ahead

While growth looks strong, hospitals face roadblocks:

- Land acquisition hurdles in congested regions.

- Regulatory bottlenecks in licensing, clearances.

- Staffing shortages—India’s doctor-to-patient ratio remains below WHO norms.

- Investor concentration—PE activity is skewed towards big players (Apollo, Max, Manipal), limiting smaller hospitals’ expansion.

Building a Future-Ready System

India’s private hospital sector is undergoing a fundamental shift:

- From metros to Tier II/III towns.

- From reactive to preventive, chronic-care systems.

- From physical-only to hybrid physical + digital care models.

To sustain momentum:

- Policy clarity on land, FDI & regulatory processes is crucial.

- Insurance penetration must deepen further.

- Skill development in healthcare workforce will be critical.

As Dr Suneeta Reddy of Apollo Hospitals says:

“Expanding insurance penetration & investing in skilling workforce will be critical to build a future-ready healthcare system that truly serves all of India.”

| Hospital Chain | Current Bed Capacity (2023–25) | Upcoming Expansion (Beds) | Capex / Investment Commitment | Geographic Focus (Beyond Metros) | Expansion Mode | Digital & Tech Initiatives |

| Apollo Hospitals | ~8,500+ beds (30% in Tier II/III cities) | +4,372 beds in 3–4 years | ₹8,000+ crore (₹6,000 crore yet to be deployed, largely internal accruals) | Gurugram, Pune, Varanasi, Lucknow, Mysuru | Mix of greenfield & brownfield | Apollo 24/7 app (teleconsults, pharmacy, diagnostics), Apollo TeleHealth rural network |

| Max Healthcare | ~4,200+ beds | +265 beds (Lucknow upgrade) + 500-bed greenfield project | ₹1,500–2,500 crore in UP; earlier ₹940 crore for Sahara Hospital acquisition | Lucknow, Shaheed Path (UP expansion focus) | Acquisition + brownfield + greenfield | Tele-ICU, remote monitoring (early pilots), integrated patient apps |

| Manipal Hospitals | ~10,600–12,000 beds (post-Sahyadri deal) | +1,400 beds under development | Temasek-led PE infusion (~$2B), additional $400M from Mubadala & partners | Maharashtra (Pune, Nashik, Karad), Karnataka, Chhattisgarh; exploring Eastern India, NCR, Telangana, Kerala | Large acquisitions (Sahyadri), brownfield + greenfield | Telemedicine, remote monitoring, hybrid care model |

| Fortis Healthcare | ~4,500+ beds | +2,000 beds (brownfield towers in Noida, Faridabad, Gurugram; Punjab expansion) | Internally funded; ₹1,550 crore via NCDs for diagnostics | Punjab (Ludhiana, Amritsar, Mohali, Jalandhar), NCR | Brownfield + targeted acquisitions (Shrimann Superspecialty, Jalandhar) | Digital linkages between Tier II centres & city specialists |

| Aster DM Healthcare | ~4,700+ beds (India operations) | +3,300 beds (2,100 organic, 1,200 via QCIL merger) | ₹1,900 crore (organic), merger synergies | South India focus, expanding to Tier II cities | Brownfield + merger & acquisition (QCIL) | Aster Health App, AI diagnostics, cloud EHR, Aster@Home (remote care) |

| KIMS Hospitals (Telangana) | ~4,000+ beds | +4,000 beds (doubling capacity) | ₹2,000 crore (internal accruals) | Telangana & southern states | Organic expansion (new hospitals) | Teleconsults, patient engagement platforms |

Punjab’s Healthcare Transformation: Demand, Disparities & Opportunities

- Demand for modern hospitals is surging due to rising incomes, health awareness & urban migration, especially in Ludhiana, Amritsar & Mohali.

- Rural Punjab (e.g., Ferozepur, Barnala) faces severe specialist shortages (doctor-patient ratio: 1:25,0001:25,000 vs WHO’s recommended 1:1,0001:1,000).

- Urban centers are referral hubs for surrounding districts, while expertise in senior care, cardiology, oncology & orthopedics is rapidly growing in places like Jalandhar, Ludhiana, Amritsar & Bathinda.

Punjab’s Hospital Investor Advantages

- Lower land & construction costs (e.g., 100-bed NABH-ready hospital in Mohali costs 15–20% less than in NCR or Mumbai).

- Over 150 medical colleges ensure a steady talent pipeline, while NRI community actively invests in Doaba-region facilities.

- Seamless policy support through Invest Punjab, plus incentives for green building, telemedicine, digital systems & PPP projects.

- Strategic deals such as Ujala Cygnus’ ₹500 crore acquisition of Amandeep Hospitals bring super-specialty care (cardiac, trauma, oncology) to underserved cities like Amritsar, Pathankot & Firozpur.

Tier 2/3 Cities—Ideal Investment Destinations & Hospital Types

| City | Hospital Type | Key Opportunities |

| Ludhiana | Super-specialty, Cardiology | Economic magnet, high patient inflow |

| Amritsar | Oncology, Cardiac, Trauma | Regional hub, high NCD burden |

| Jalandhar | Senior care, Orthopedics | Aging population, residential facilities demand |

| Mohali | IVF, Respiratory, Multi-specialty | Clean air, strong regulatory framework |

| Bathinda | Cancer, Cardiac, Diagnostics | PPP-driven specialty projects |

| Pathankot, Mansa, Sangrur | Multi-specialty | Underserved catchments, rising income |

| Ferozepur, Barnala | Low-cost care, Satellite centers | Rural referral, affordable models |

Government & Private Sector Initiatives

- Punjab government has successfully built super-specialty PPP hospitals—changing landscape in Mohali & Bathinda & incentivizing private players for further expansion.

- Apollo, Fortis, Ivy, SPS Apollo, Indus Hospital & more, are targeting both metro-adjacent & non-metro regions for new projects (some aiming for 1000+ new beds & allied colleges).

Investment Challenges & Solutions

- Workforce Shortages: 80% of specialists reside in metros; Punjab’s tier 2/3 cities need better retention schemes & training programs for healthcare workers.

- Infrastructure Gaps: Transportation, power reliability & medical equipment maintenance remain critical gaps in rural zones—solutions include mobile units & telemedicine, both gaining policy support.

- Financial Solutions: Population in these cities is price-sensitive; models include cashless insurance, financial innovation & donor involvement (NRI, CSR, etc.).

Conclusion

What began as a lifeline for a teacher in Lucknow is now a national restructuring of healthcare delivery. With ₹35,000+ crore in upcoming investments, 30,000 new beds & digital platforms scaling care access, India’s corporate hospital chains are shaping next decade of healthcare infrastructure.

Big question isn’t whether this expansion will happen—it already is. Real test will be sustainability: Can India’s private healthcare build inclusive, affordable & tech-driven systems that serve not just metros, but hundreds of millions living in smaller cities & towns? Answer will define future of health in India.

References

- “How India’s hospital chains are entering an aggressive phase of expansion in Tier II/III cities,” Business Today, 28 July 2025. Business Today

- “New Capex Cycle to Boost Corporate Hospital Bed Capacity by 35-40% Over 3-5 Years,” CareEdge Ratings report. It projects that top listed hospital chains will increase bed capacity by ~35-40% in 3-5 years, driven by demographic shifts, insurance expansion and rising incomes. CARE Ratings

- “Fresh capex to boost hospital bed expansion by 35-40% in 3-5 years,” Business Standard, based on a CareEdge Ratings report: corporate hospitals to expand beds by 35-40%, ARPOB & occupancy rise expected, margins to remain stable. Business Standard

- ICRA report: Eleven listed hospital players and two large unlisted players are expected to add ~14,500 beds over FY2026–FY2027 with total capex of ~₹30,000-32,000 crore, even while debt coverage metrics remain healthy. ICRA

- “Health insurance coverage in India projected to reach 50% by 2025,” CareEdge Ratings insight: insurance, medical seats and bed capacity rising; full coverage still facing gaps.

- WHO / peer-reviewed studies about non-communicable diseases (NCDs) burden in India:

S. Sahu et al., “The burden of lifestyle diseases and their impact on mortality” — NCDs and injuries responsible for ~52% of fatalities in India.

MK Pati et al., “A narrative review of gaps in the provision of integrated care …” — NCDs contribute ~60% of all deaths in India, large out-of-pocket expenses, especially for outpatient care.