In case you have been living under a rock for past few months, lot of discussions have been going on Foreign Exchange reserves of India in news lately, because they have been shrinking at a pretty sharp pace. The reason for this sharp decline is, firstly, the RBI has been selling dollars to tackle the sharp fall in the exchange rate, as investors start buying US short term bonds and sell Indian securities. Secondly, we buy a lot of oil and spend dollars for that.

The rupee has almost touched 82 mark, not because there is something fundamentally wrong with the Indian economy, but the dollar has just increased in strength with respect to all of the currencies in the world. The side effect of this high dollar index is that American industries are getting outpriced in the global markets, and become uncompetitive in the short run, but that is a discussion for some other day. The argument is whether the RBI is doing too much to stop the decline of the Rupee, by selling its forex reserves?

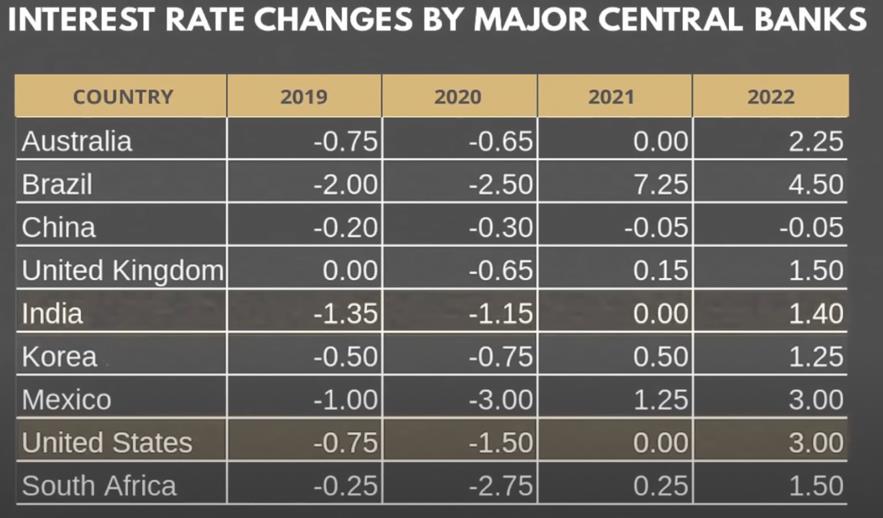

Indian Forex reserves have fallen by almost 85 Billion dollars in the current calendar year, this is the steepest decline in the reserves since the war started in Ukraine, the pace has picked mostly in the last two months. One reason, primarily, is that the dollar index has increased, the federal reserve bank of US has been aggressively raising the interest rates. Among all central banks raising rates to tackle the red-hot inflation, US is far more aggressive in raising rates.

Dollar dominated assets have surged, the other currencies have faced depreciation pressures.

Some people have started comparing this process to the 2013 taper tantrum, or the financial crisis in 2008. During the taper tantrum (2013) the US fed chairman indicated that they will start tapering of bond buying program. This led to huge outflows of dollars leading to Rupee depreciation. The Rupee depreciated by almost 16 percent during that time. RBI didn’t tackle the downfall of rupee so there was no sharp decline in our forex unlike what has happened now. During taper tantrum the reserve bank raised the rates aggressively to stop the outflow of dollars, however in these times RBI has been using the forex, as they were on a record high (680 Billion Dollars).

So how does one decide how much forex is enough?

We always read about that we have forex of 6 months of imports etc. Sri Lanka had forex for 1 weeks of imports few months back, Pakistan had 1 month of forex etc.

The international monetary fund (IMF) has come up with set of indicators to decide the adequacy of reserves for different type of economies whether you are a closed economy, emerging market economy or you are an advanced economy.

Traditionally there are three metrics to assess the reserves adequacy.

- How much of the reserves can provide cover for imports – The thumb rule is that reserves should cover 3-4 months of imports. This is true for closed economies. These economies don’t have financial linkages internationally. The capital flows are sufficient to finance the imports. Like what they have in Brazil, where they have current account deficits, but their capital inflows from FIIs and FPIs are quite robust.

The second indictor is more applicable for emerging economies. –

- Whether your reserves are sufficient to cover short term debt (External Debt) – If your reserves are sufficient to cover 100 percent of short terms debt servicing, it means reserves are enough, for countries like India. According to RBI, India’s Short term debt to Forex is around 41%, so it means we are ok.

- What is proportion of reserves to money supply – This metric is important when the crisis rises up due to outflow of deposits. Like, in case the inflows of deposit dry and out flow of resident deposits starts happening. To contain that kind of crisis, the reserves should be enough to capture your money supply. Money supply means your currency and deposits.

- Forex reserves to the GDP ratio – At our peak of 680 billions of reserves our ratio was 21% of GDP , right now it’s around 17 % of GDP. We should compare these ratios to what they were during the financial crisis or taper tantrum.

Recently a poll conducted by Reuters was released which said its median results show that forex could fall to 520 billion at end of financial year, and that would be enough for imports of 8 months or so, which could be equal to “danger mark”.

These things tell you two things: where does the dollar go from here, how much RBI should try to stop the declining rupee, and is it even worth to sell more?

If the US Fed keep on increasing the rates, like what they are saying as per their forward guidance, US FED is expected to raise rates by 120 Bps this year and not reduce the rates in next year too. Based on this, it is expected the dollar will continue to rise, and rupee will fall. RBI should not sell more dollars to keep on defending Rupee to keep Rupee at some artificial rate just to keep political environment calm.

The Rupee slide in the near term will not harm the economy, hopefully the current account deficient as per of GDP (currently at 2.8% of GDP) might be getting better, due to export becoming more competitive. Also, due to the global slowdown the commodity prices will come down too, so the import bill will also come down.

Written By: Ankur Kushwaha, Sr. Consultant, Invest Punjab | Govt. of Punjab.

DISCLAIMER: Views expressed are personal.